Satellite Launch Vehicle Market Growth, Size, Share, Analysis, Forecast 2025–2032

- Rishika Chavan

- Aug 20, 2025

- 4 min read

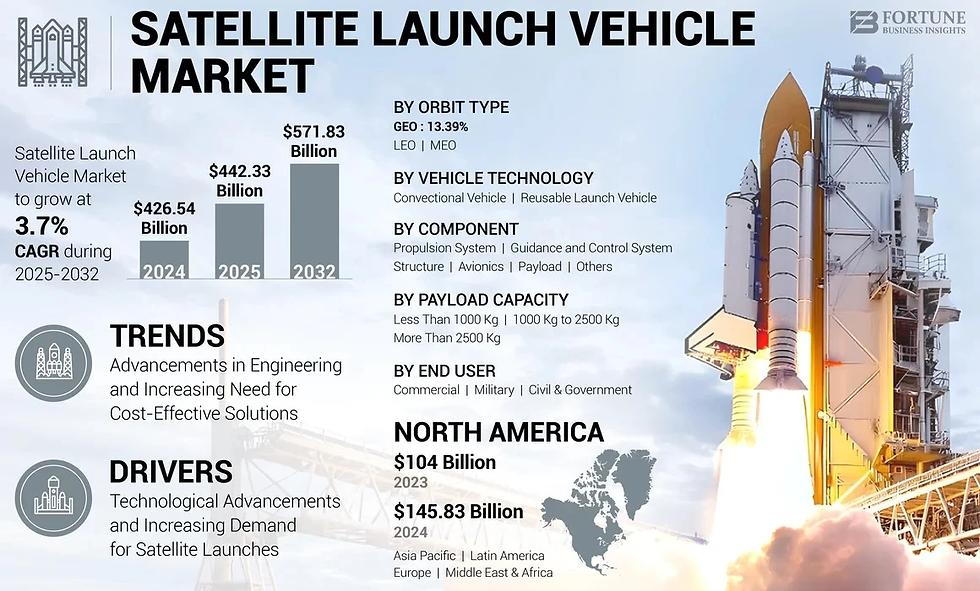

According to Fortune Business Insights™, the global satellite launch vehicle market was valued at USD 426.54 billion in 2024 and is projected to grow from USD 442.33 billion in 2025 to USD 571.83 billion by 2032, exhibiting a CAGR of 3.7% during the forecast period. The market expansion is fueled by the rising demand for satellite deployments in commercial, military, and civil applications, alongside advancements in reusable launch technologies, miniaturized satellite designs, and AI integration.

The demand for satellite launch vehicles is accelerating due to the increasing role of satellites in communication, navigation, Earth observation, weather forecasting, and defense. Modernization of platforms, digital transformation, and ongoing innovations are reshaping the market landscape. For instance, in November 2024, Boeing delivered two additional O3b mPOWER satellites for SES, showcasing advanced software-controlled payload technology for flexible bandwidth allocation.

Key Companies Profiled

Airbus S.A.S (Netherlands)

Arianespace (France)

The Boeing Company (U.S.)

Rocket Lab (U.S.)

Mitsubishi Heavy Industries, Ltd. (Japan)

Northrop Grumman (U.S.)

Lockheed Martin Corporation (U.S.)

Blue Origin Enterprises, L.P. (U.S.)

SpaceX (U.S.)

ISRO (India)

Major players such as SpaceX, United Launch Alliance, ISRO, NASA, and CASC are contributing significantly to market growth through technological advancements and increasing satellite launch frequency.

Information Source:

Market Segmentation

By Vehicle Technology

Conventional Vehicle: Accounted for the largest market share in 2024, supported by technological upgrades and government investments.

Reusable Launch Vehicle (RLV): Expected to be the fastest-growing segment (2025–2032). Reusable launch technologies reduce costs and enhance mission flexibility. For instance, in September 2024, ISRO approved the development of its Next Generation Launch Vehicle (NGLV), designed for reusability and heavier payloads.

By Orbit Type

Low Earth Orbit (LEO): Fastest-growing segment, driven by demand for low-latency and cost-effective communications. For example, Geespace launched 10 LEO satellites in September 2024 to expand its mega-constellation.

Geostationary Orbit (GEO): Second-fastest growing segment, driven by communication services and government initiatives.

Medium Earth Orbit (MEO): Stable demand for navigation and positioning services.

By Payload Capacity

Less than 1000 kg: Fastest-growing segment due to rising adoption of CubeSats and small satellites for military, communication, and research. In April 2024, SAIC and GomSpace collaborated to develop an AI-powered small satellite.

1000 kg to 2500 kg: Second fastest-growing, fueled by medium-size satellite launches.

More than 2500 kg: Stable demand for large payload launches.

By Component

Propulsion System: Fastest-growing segment, with innovations in green propulsion and electric systems. For example, in September 2024, Benchmark Space Systems received USD 4.9 million to develop ASCENT monopropellant propulsion systems.

Avionics: Second fastest-growing segment, as advanced GPS and navigation systems enhance mission reliability.

Other components include structure, payload, and guidance systems.

By End User

Military: Fastest-growing segment, driven by satellite investments for defense, surveillance, and secure communication. India announced USD 3 billion investment in space defense programs in March 2024.

Commercial: Largest share in 2024, supported by growing satellite services for communication and broadband.

Civil & Government: Ongoing investments in space exploration and scientific research.

Market Dynamics

Drivers

The satellite launch vehicle market is primarily driven by the rising demand for communication, Earth observation, and scientific satellites, which continues to fuel the need for reliable launch services. The rapid growth of small satellite and CubeSat missions is further accelerating this demand, as these platforms require cost-effective and flexible launch solutions. Increasing private sector participation, led by companies such as SpaceX and Rocket Lab, is transforming the industry with innovative reusable rocket technologies and reduced launch costs. Additionally, government space initiatives and higher defense spending are strengthening the global market, with national space agencies focusing on independent launch capabilities and strategic space programs.

Restraints

Despite strong growth prospects, the market faces several restraints. High research and development costs represent a significant challenge, particularly for smaller players attempting to compete with established providers. Engineering and refurbishment issues linked to reusable launch vehicles add further complexity and raise operational risks. Moreover, the risk of launch failures poses both financial and reputational setbacks for companies. Another restraint is the supply-demand imbalance caused by overcapacity in certain regions, which can limit profitability and disrupt launch schedules.

Opportunities

On the other hand, the industry is witnessing emerging opportunities that could redefine its trajectory. The integration of artificial intelligence in mission planning and space debris management has the potential to enhance safety, efficiency, and operational reliability. Advancements in additive manufacturing, particularly 3D printing, are enabling cost-efficient and rapid production of components, reducing overall development cycles. The growing adoption of sustainable practices such as green propulsion systems and recyclable materials reflects the industry’s commitment to environmentally responsible operations. Furthermore, the expansion of the small satellite and CubeSat markets offers consistent opportunities for dedicated and rideshare launches.

Challenges

Nevertheless, the market continues to grapple with several challenges. Limited payload capacities restrict the competitiveness of some systems compared to next-generation heavy-lift vehicles. While reusability has become a major focus, the high costs and technical difficulties associated with it remain barriers to widespread adoption. Demand forecasting also poses a challenge due to longer satellite lifespans and changing mission requirements. Additionally, overcapacity issues, particularly evident in regions such as India with ISRO’s current infrastructure, can lead to inefficiencies and delays, further complicating market growth.

Market Trends

Advanced Propulsion Technologies: Increasing shift toward eco-friendly fuels such as green propellants. For example, Bellatrix Aerospace tested its non-toxic Rudra propulsion system in January 2024.

AI and Automation: Enhancing efficiency in launch planning, trajectory optimization, and payload integration. In September 2024, Proteus Space announced plans to launch the first AI-designed ESPA-class satellite in 2025.

Regional Insights

North America: Largest market share (USD 145.83 billion in 2024). Driven by U.S. defense spending, NASA investments, and strong private sector involvement.

Asia Pacific: Fastest-growing region. Countries like China, India, and Japan are advancing national security initiatives and fostering private space startups. For example, India launched RHUMI 1, a reusable hybrid rocket, in August 2024.

Europe: Second-fastest growing region. ESA expanding investment in commercial-led launch services.

Middle East & Africa: Moderate growth with new programs from UAE, Saudi Arabia, and Israel. Yahsat selected SpaceX for satellite launches in July 2024.

Latin America: Growth led by Brazil, Argentina, and Colombia through new partnerships, such as Brazil’s 2024 agreement with China’s National Data Administration and SpaceSail.

Recent Developments

November 2024: Rocket Lab USA signed a multi-launch contract for its Neutron medium-lift rocket with a commercial satellite operator.

November 2024: ESA and ArianeGroup signed contract addendums worth USD 232.47 million to advance Prometheus engine testing and reusable rocket demonstrator Themis.

Comments